Mutualism

Sara Horowitz is a lawyer who founded the Freelancer's Union to help provide a safety net for the many independent workers in nontraditional employment relationships. Freelancers have been at the forefront of the disintegrating safety net for decades. But now, with the social safety net all but gone, we are all impacted.

Named MacArthur Fellow and having served on the Federal Reserve Board of New York, Horowitz has held labor interests as her north star throughout her career. This former labor organizer and public defender comes from a lineage of organizers. In the early 20th century, Horowitz's grandparents were both leaders in the ILGWU, one of the largest unions in the country that represented 15,000 garment workers.

In her book Mutualism, Horowitz describes how these early unions not only organized strikes but also functioned as holistic organizations, meeting the needs of their community members. To these early unions, a worker was not simply an economic unit but a whole human being who needed healthcare, art, leisure, and education. Union leaders were sophisticated in running businesses to meet members' needs. They founded healthcare clinics, built cooperative housing, and started credit unions, all built from scratch because no safety net existed. The profits from the investments and businesses of the early unions went back into the communities to enrich workers' lives.

Other than labor organizations, Horowitz cites other great examples of mutualist organizations that changed history through institutions built on reciprocal obligation. These include the Civil Rights Movement, religious organizations, cooperatives, Black community "associations”, credit unions, and mutual aid societies.

What makes an organization mutualist is that it has a social purpose (serving a community), an independent economic mechanism (way of making money), and a long-term focus (built to outlast its members.)

Mutualist ecosystems were the force that built the safety nets, argues Horowitz – not charities or government – and can remake them. The national safety net, beginning with the New Deal, which enshrined protections into law, is not only a triumph of big government. Horowitz tells the story of how Roosevelt helped the largest mutualist organizations of the time grow and thrive.

But, she says, we have lost our mutualistic muscle memory and encourages all of us to build it again. Horowitz believes both major political parties acted as two sides of the same affluent coin. The political right cut taxes, promoted deregulation, and worked to dismantle unions directly. The left came to see government as the only institution capable of solving problems and abandoned unions, which were the original architects of the New Deal. We must support both government programs for people who are unable or no longer work and, also, grow strong, local mutualist institutions for workers, regardless if they are lower wage, blue collar, or professional.

We must invest in the mutualistic sector again and develop a keen awareness of our obligations to one another. We shouldn't wait for the government: Mutualist leaders will solve problems locally, build economic independence, and be empowered to petition the government to make regulatory changes that will let mutualist organizations thrive.

Horowitz asks, "What if we were able to replicate what the early unions and mutualist organizations were able to accomplish in the 1910s and '20s, but use technology to scale it to a degree that those early American innovators could never have dreamed of?"

The new safety net will reflect who we are. We live in a decentralized economy; the safety net will reflect that. Traditional business and big government strategies no longer fit. The mutualist sector, which collectively has a huge worker base and vast revenue streams, already exists. This collectivity can join forces to empower existing mutual organizations and create the conditions to support new ones.

Because communities and organizations based upon mutualism make decisions that aim to maximize the benefit for everyone, Horowitz states that by definition and design, they are deliberative and slower. They base their decisions upon diverse opinions and beliefs, made with a longer term view to ensure continuity.

How can we create mechanisms to support entities that will return us to a collectively healthier way of living and relating to each other?

Mutualist organizations can join forces to encourage public policymakers and private capital to invest in them. What might this look like? For one, there is no consistent lending source for social purpose organizations because they aren't run in the two recognized ways – for maximizing profit or as a charity. Unlike conventional businesses, mutualist organizations reinvest profits into their communities rather than pay investors. We must educate lenders to recognize that while these businesses will ultimately make money, the investment is primarily about helping communities help themselves in solving social problems.

Horowitz notes that without "patient investments," mutualist entrepreneurs must choose between taking charity or putting profits over their communities' needs. There needs to be capital that does not prioritize shareholders, who are passive investors and are not adding to communities.

Horowitz makes the case that governmental policy can help create the market conditions for the right kind of lending by earmarking funds for these enterprises and offering tax deductions for investment in mutualist organizations. We already do this for foundations and nonprofits, which, collectively, have trillions of dollars. The government has always created, regulated, and advantaged markets through its tools. Horowitz reminds us that after the 2008 financial crisis, the Federal Reserve injected copious amounts of money into quantitative easing to remove toxic assets from banks to stabilize them.

Horowitz argues that we need to change the direction of the river of capital. To strengthen the mutualist sector, we must shift from an extractive lending model to one that facilitates recycling capital back into communities. She writes, "Imagine if there was ready funding available to start a cooperative daycare with other parents in your community. Or if it was just as easy for an entrepreneur to get money to build a new, low-cost, freelancer-focused mutual insurance company that was designed to serve you as it is for entrepreneurs to get money to scale for-profit startups designed to make investors rich."

Horowitz goes further: What if the government required foundations to earmark a small amount, say one percent, to mutualist organizations? Or even to the banks, who, during crises, get vast amounts of “patient capital” from taxpayers? Or the same for venture capital firms who get billions of dollars to invest from mutualist organizations like unionized pension funds and university endowments? Why can't they give one percent back to the capital markets they pull from by investing in these organizations?

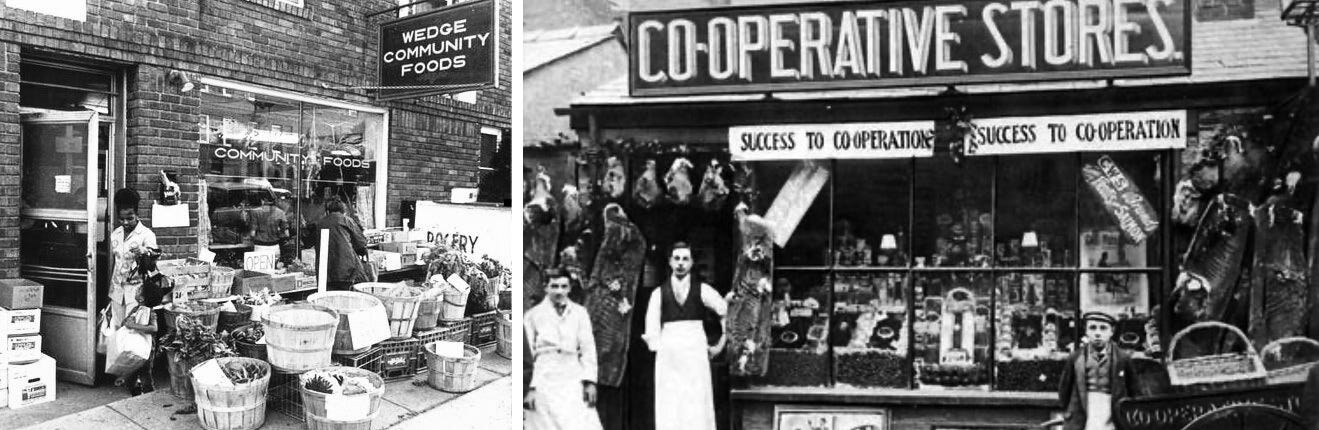

As individuals, we can support mutualist organizations near us. You might start with shopping at a food co-op near you or banking at a local credit union. Joining a local club around your interests – cooking, running, writing, advocacy – is another way to connect in the spirit of mutualism.

Horowitz suggests that if you identify a community need, try to find an organization already finding solutions and support it. If you can't find one that meets your identified needs, consider building one yourself. She encourages us to step up and become mutualist leaders. If we cannot lead, we can play an important role by supporting mutualism in other ways.

Horowitz offers a lovely example of mutualism from her childhood in Brooklyn Heights. Her parents were part of a babysitting cooperative that used Monopoly money to pay for babysitting. When members didn't have any left, they babysat to get more. This cooperative knew one another, and its existence grounded the children in the neighborhood. Neighbors cultivated a vibrant community because they identified a need. They could not afford to pay for childcare. As a result, they built a community to find a solution, and the children benefited by feeling the community's collective care.

Mutualism starts small: No movement began with the idea of becoming a movement. Effective mutualist organizations all start with relationship building, listening to community members, and baby steps. Follow your intuition, and don't worry about any particular outcome. Stay at it and keep connecting!

Mutualist organizations can connect with other mutualist organizations. In building a complex web of mutual obligation, we will move the needle toward social change. Horowitz envisions a vast ecosystem where we are all helping ourselves and one another by taking responsibility for our destinies.